If you're planning on buying a home in Southern California, you're likely expecting an interest deduction on your mortgage. But, under the new GOP tax plan, your mortgage can't exceed $750,000 - lowered from the previous limit of $1 million.

If they're looking at buying a $1.2 million house and they put down 20 percent, their mortgage will be $1 million so they will have to know that on that $250,000, they won't be getting the tax break they got before.

In a housing market like California's, where prices are twice the national average, you could find yourself paying more. There's a shortage of homes on the market so it's going to take a little time for the buyers to absorb this information. Typically we see a slower time during the winter time. But I think by spring time, people will adjust to the new tax plan and we'll be back to normal.

Those impacted will be people purchasing more expensive homes. The biggest tax overhaul in 30 years also limits the deduction on state and local taxes, which include property taxes, to $10,000 a year. In California, where we have state taxes and property taxes, were going to find that a lot of people who have counted on the tax deduction for mortgage interest and property taxes are now going to not have that tax deduction. Therefore, their housing cost is going to be a little bit higher than it's been previously.

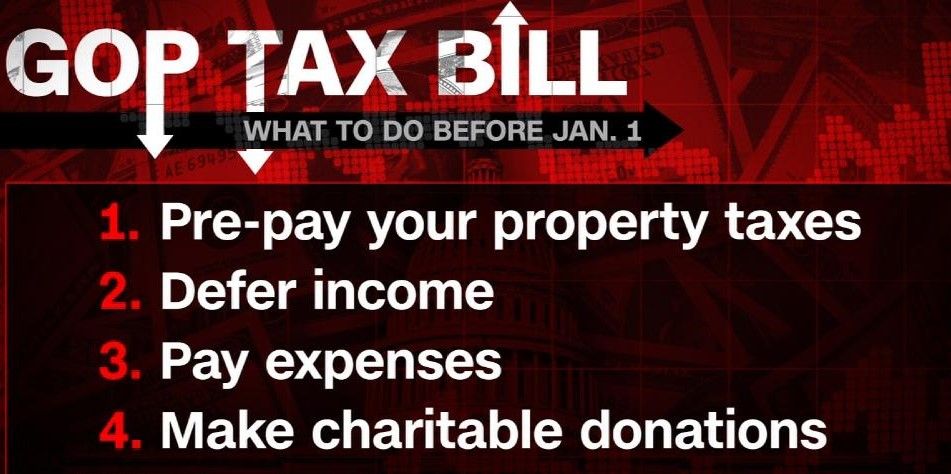

Tax experts are encouraging all Americans to consult with their accountant now to determine whether paying their January mortgage payment or upcoming property taxes before the end of the year would save them money.